Published: 17 October 2018

Share of cultural fields in employment in the national economy was still falling, but the share of value added was growing slightly in 2016

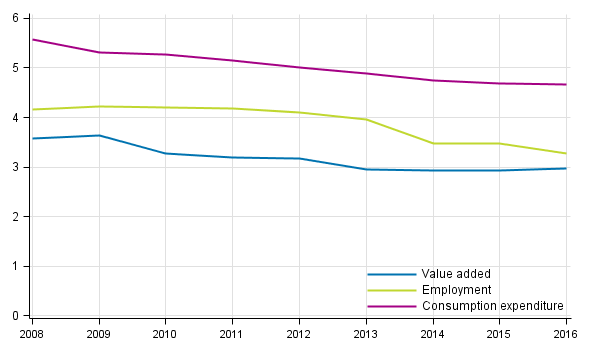

In 2016, the share of culture in the economy was slightly bigger than in the year before, or 3.0 per cent of gross domestic product (2.9 per cent in 2015). In previous years, the tendency has been falling both in production and especially in employment. The direction appears to have turned for production, although in employment the share of culture continues falling. The games industry also grew in 2016, even though the growth rate seems to have slowed down clearly. Most of the activity of the games industry remains outside the limitations of the actual culture satellite, but separate calculations have been made on the games industry for this release.

Percentage share of cultural industries in the national economy in 2008 to 2016

Measured in current prices, the value added of culture was in 2016 clearly higher than in 2015, but the share of culture in the value added of the whole economy grew only slightly, because the value added of the entire economy also grew. In many industry groups, value added was either unchanged or had grown slightly and somewhat bigger growth was visible particularly in the industry groups ‘publishing and retail sale of books’, ‘recorded media’ and ‘arrangement of cultural events’. On the other hand, a clear decrease was visible in the industry groups related to the manufacture and sales of entertainment electronics, and radio and television.

In 2016, the share of combined consumption expenditure of culture in all consumption expenditure remained unchanged. General government's consumption expenditure of culture remained at current prices on level with the previous year and private consumption expenditure rose slightly. But because consumption expenditure increased on the level of the whole economy, the share of culture in consumption expenditure was the same as in the previous year.

In 2016, the share of culture in employment was 3.3 per cent. The share of culture in employment has been clearly higher than its share of value added or output, but the difference has constantly narrowed down. The labour domination of culture is affected by the relatively low pay level, part-time work and absence of big companies producing large profits. The absolute decrease in the number of employed persons in cultural industries that has continued since 2008 appears to go on further.

Culture has conventionally been regarded as an activity that balances economic cycles, whose role usually grows somewhat during a downturn, because it includes several permanent elements. The share of non-profit and public activities is significant and most engaged in the cultural field do not even imagine they will get rich by their activity. Culture is produced for its own sake in bad economic times as well, even without profit. The prolonged economic downturn has, however, been visible in both cultural production and in its consumption; also when it comes to culture, people look for more inexpensive alternatives when the economy is tight, and the rise of the economy is not actually visible in culture yet, although particularly in production it would appear that the long lasting fall has ended and maybe it will even turn into growth.

Although the share of culture in the economy has been falling on the long term, culture still has a fairly important role in the national economy, because its share of consumption is nevertheless nearly five per cent and its share of employed good three per cent.

The games industry is growing fast and remains mostly outside the culture satellite.

Beside the culture satellite, Statistics Finland has also calculated total development between 2008 and 2016 for the games industry that has received much publicity. The games industry can, at least broadly understood, be seen to belong to culture, but most game developer companies are working in the industry of programming, which is not included in the culture satellite calculations.

The growth in the games industry that started in 2013 is still continuing, although its rate appears to have slowed down clearly from the wildest years. The growth in the Finnish games industry is strongly linked to a few individual enterprises.

If games industry enterprises belonged to the culture satellite, the value added of culture in 2016 would be nearly 20 per cent higher than with the present limitation. Games industry enterprises would not have a significant effect on employment in the cultural industries, but employment would in practice remain at the same level. For the entire economy, the games industry does not, at least yet, have a huge significance, although its share of GDP has in a few years well over tripled from close on 0.2 to 0.6 per cent.

The statistics on Culture Satellite Accounts depict the economic significance of culture, using the concepts and methods of National Accounts. Data according to the Standard Industrial Classification TOL 2008 have now been released for the years 2008 to 2016 in accordance with the ESA2010 system

The data for the Culture Satellite Accounts are published on the statistics website as database tables.

Source: Culture Satellite Accounts, Statistics Finland

Inquiries: Katri Soinne 029 551 2778, kansantalous@stat.fi

Director in charge: Ville Vertanen

Publication in pdf-format (219.1 kB)

- Tables

-

Tables in databases

Pick the data you need into tables, view the data as graphs, or download the data for your use.

Appendix tables

Updated 17.10.2018

Statistics:

Culture satellite accounts [e-publication].

ISSN=2323-9905. 2016. Helsinki: Statistics Finland [referred: 25.7.2026].

Access method: http://stat.fi/til/klts/2016/klts_2016_2018-10-17_tie_001_en.html